The second part of Series “Current temptation, future frustration“. This series is based on the companies which are currently darling of the market and many trying to catch such opportunities but it has a probability to become a reason for future frustration. It can wipe out the majority of gains in wealth. I am trying to put some of the number-crunching facts by which we can identify ongoing issues in the companies and can save our wealth.

I am starting this series with one of the company which is engaged in manufacturers of Wind Turbine Generators (WTGs) in India, has a 52 weeks low price of Rs.16 and LTP is Rs.48.15. This company has rewarded ~3.01x of return in a year.

Let’s start looking at the numbers.

We can see that the company has a declining trend of revenue, operating & PAT level also incurring losses. But the company has delivered a good return in a year so it might be possible that the company has a strong balance sheet.

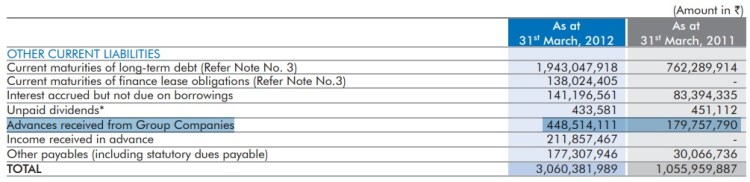

When we look at the balance sheet then I got shocked. The company has trade payable, inventories and receivables are higher than sales. Also, the company is getting higher advances from its customer which is again higher than sales so that the company should have a monopoly and everyone wants its products only. But then why revenue keeps on declining?

Cash conversion cycle of the company is of 497 days in FY20 means its take almost 1+ years to convert to cash. Even the company has receivables, inventories and payables as a % of sales are 174%, 131% and 139% respectively.

When I have looked at the related party transaction then Rs.450 cr of sales in FY20 and Rs.648 cr of sales in FY19 done through related parties which are 59% of sales in FY20 and 45% in FY19.

Another part, when we look at the advances from customers then all are from related parties only. This trick is used by the company to show slightly better CFO. Also, receivable from related parties is 20.49% of total receivables in FY20 and 18.40% in FY19. And if we look at the receivable as a % of sales to related parties then it is 60.16% in FY20 and 46.31% in FY19. Now, I am curious that related parties have ~Rs.1100 cr of the fund to give as an advance but do not have Rs.270 cr to pay for receivables.

When we look at the exposure of the company to related parties then it is worth of Rs.865.46 cr in FY20 and Rs.708.10 cr in FY19 which is 16.35% in FY20 and 14.94% in FY19 of total balance sheet size. These related parties are making losses.

The company has Cumulative CFO < Cumulative PAT which shows difficulties to convert PAT into Cash Profit. Also, CFO is artificially boosting through advances from customers which is from the related parties.

This entire series is based on past available data and ignored the future development in companies and the stock market always looks at the future.

Disclosure – Companies mentioned in the article are just for an example & educational purpose. It is not a buy/sell/ hold recommendation.

This series contains learning from books –