During my course at Flame University “Art of Investing with Neeraj Marathe”, Mr.Durgesh Shah Sir has suggested me to read a book which is “Big Mistakes”. So that I am hereby starting to write my learning from the book.

We make many mistakes in life and learn from those mistakes. We keep focus on does not repeat the same mistakes again and again.

My Guru always quotes that “If we focus on avoiding mistakes then we won half of the battle.” We always cannot keep on making mistakes and learning from it but also we can learn from others mistakes which we can avoid during our journey.

Learning from others mistakes and experience is the easiest way to learn and grow.

I am hereby starting my learning from mistakes made by well know investors. Upcoming series will be going to include learning from the book “Big Mistakes”. I am grateful to Michael Batnick – author of the book.

The first article of the series, I start with Mr. Benjamin Graham who is a father of a value investing. He has given a new direction to the investing field.

Mr. Graham is a guru of Mr. Buffett and we cannot imagine investing field without Mr. Graham. Few biggest gift from Ben Graham to the investing field are Margin of safety, the difference between price & value, calculation of value to the business, etc.

Many a time, we think that stocks fall ~40-50% from the high price, we should start trying to catch “falling knives” (Such terminology is widely used by so-called professionals). But we should focus on the value of the particular business rather focus on the high price and current price. During recent fall to the stock market, many of the people started picking stocks just because they fall much from the high price.

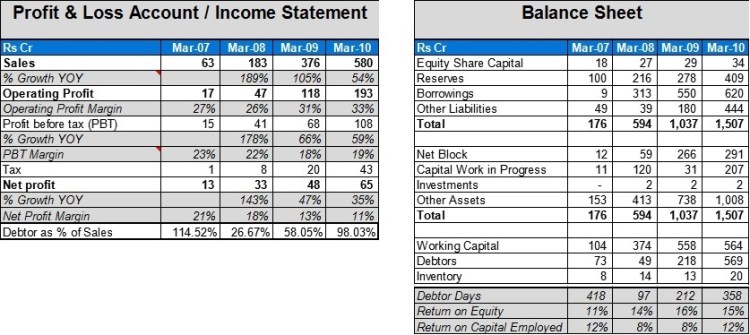

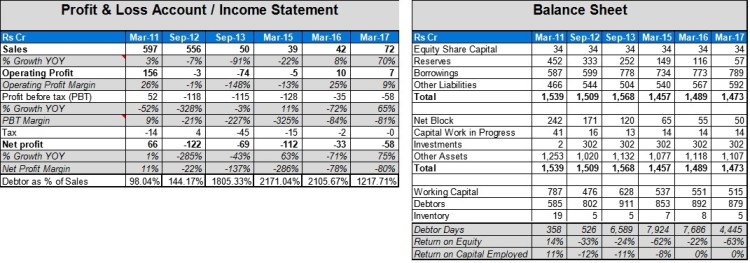

Indian companies examples

One of the media & Entertainment Company which is falling by ~51% from its high price but the company is making losses, negative CFO, management is taking a higher salary and also giving a loan to the subsidiary companies.

One of the companies which are into the DTH services and that company fall by ~79% from its high price. The company is making very little profit, very little FCF, huge debt, negative ROE% and where value can be still very less.

Such a fall in price does not make it attractive to buy which has very little or no value.

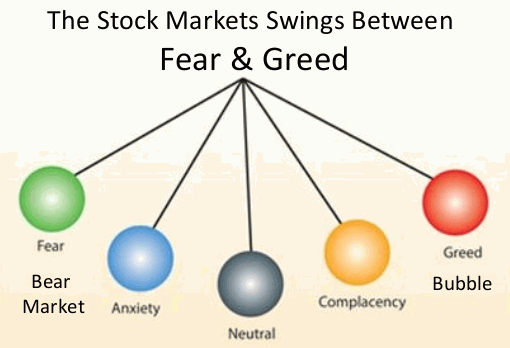

The market always works in a pendulum and people generally forget the nature of the pendulum. The pendulum always moves towards both extreme directions.

Whenever pendulum moves towards the bullish extreme, many of us forget that such situations will not stay forever. Many of us forget about the risk which involves during the bull phase. And start taking higher risk for generating higher returns; which invites a further huge amount of risk. At bullish sentiment, people generally buy assets at the highest valuations multiple and that invites the risk to the particular asset class. This scenario has a very high chance of getting damage to our wealth compared to generating a higher return.

Reverse to such scenario, whenever the pendulum moves towards extreme bearish phase, then generally people start recognizing the risk and start avoiding to invest in the particular asset class; which take out the risk from that particular asset class. Such a scenario is the appropriate time for capturing the opportunities because in such scenario we have very less chance to lose.

When people warmly accept any securities then the price will go far from the value and when people avoid or hate any securities then the security will fall in its value.

Mr. Graham has a strategy to purchase undervalued securities and shorted overvalued securities which have made him successful. Mr. Graham has started with $450000 and which he turns to be $2500000 in just three years.

During the last month of the year 1929, Dow Jones has started going down and Mr. Graham has started to cover his short positions and shifted to preferred stocks by considering prices are low. But the calculation of Mr. Graham went wrong and he lost 20% while Dow Jones down by 17%. After this Mr. Graham has considered that market has made the bottom and he used to leverage money to boost profit but again his calculation went wrong and he lost 50%. During the year 1929 to the year 1932, Mr. Graham has lost 70% of his money.

My learning

We should not take leverage to boost up our profits from the market, we cannot measure the madness of the market. I have implemented this learning from the mid time of my investment career and I have parked my money where I am convinced to park. I have never taken a leverage position rather I have to keep liquidity with my portfolio (I was holding ~73% liquidity in my portfolio during January – 2018 and currently having ~65% liquidity position). I have always focused on capital protection over the missing out of opportunity.

An example of one the biggest wealth creator company of the Indian stock market—

Read for more detail: Big Mistakes: The Best Investors and Their Worst Investments by Michael Batnick