The tenth part of Series “Once a darling, now an evil”. This series is based on the companies which were once upon a time darling of the market and now, it has wiped out the majority of all those gains. I am trying to put some of the number-crunching facts by which we have identified ongoing issues in the companies and have saved our wealth.

I am starting this part with one of a jewelry company that has an all-time high price of ~Rs.649 in 2013 and now last traded price at Rs.1.05.

In the first instance this company having huge sales and profit growth. This creates a temptation to buy with missing out of the opportunity. But after the series of articles, we know to not get tempted with sales & PAT growth.

So, we go deeper ….

Huge debtor days, Debt/equity increasing so RoE% is due to the higher leverage.

I would like to go further detail of it.

If we look at the common size balance sheet then the majority part of the assets side was other assets that have receivables & inventories. Also, cash getting reduces and borrowings getting higher. Also, when a company growing at a higher rate then what is the need for higher borrowings after using good cash balance?

The company got debt at a lower rate. Curious and that is also at the time of higher interest rate. Also, the company has to pay lower taxes. Wow… lower interest rate and lower taxes.

The company has FCCB which is a more dangerous kind of foreign debt.

Negative CFO in two years and also if we compare cumulative CFO with cumulative PAT then CCFO<CPAT.

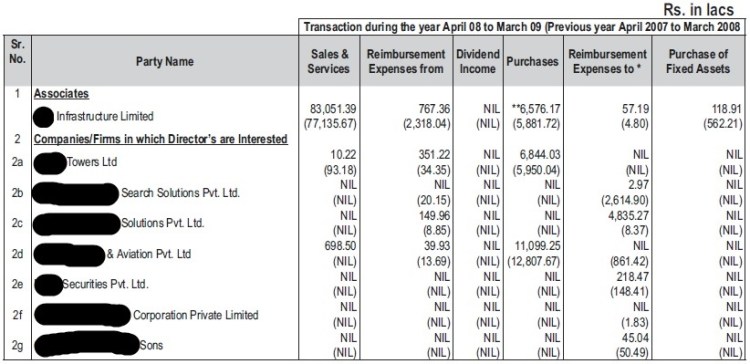

The company owns ~39 subsidiaries and associates companies which can be suspicious.

Company has given ~Rs.1400+ cr of loan and advances to subsidiaries companies on interest-free basis and repayment is beyond seven years.

Disclosure – Companies mentioned in the article are just for an example & educational purpose. It is not a buy/sell/ hold recommendation.

This series contains learning from books – Financial Shenanigans Quality of Earnings The Financial Numbers Game Creative Cash Flow Reporting